4

Shareholder Value Creation in Japanese Pharmaceuticals

2. JAPANESE PHARMACEUTICAL COMPANIES HAVE

NOT MET INVESTORS' EXPECTATIONS

Expectations and gaps from the perspective of investors and shareholders towards Japanese

pharmaceutical companies:

As mentioned above, the evaluation from investors towards the deteriorating performance of Japanese pharmaceutical

companies is generally not high. In this section, we will detail how investors and shareholders evaluate Japanese

pharmaceutical companies.

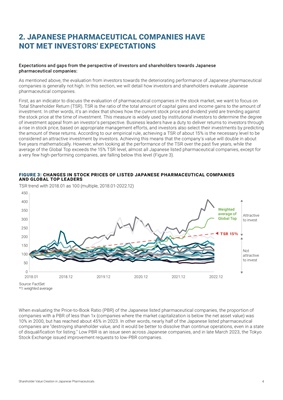

First, as an indicator to discuss the evaluation of pharmaceutical companies in the stock market, we want to focus on

Total Shareholder Return (TSR). TSR is the ratio of the total amount of capital gains and income gains to the amount of

investment. In other words, it's an index that shows how the current stock price and dividend yield are trending against

the stock price at the time of investment. This measure is widely used by institutional investors to determine the degree

of investment appeal from an investor's perspective. Business leaders have a duty to deliver returns to investors through

a rise in stock price, based on appropriate management efforts, and investors also select their investments by predicting

the amount of these returns. According to our empirical rule, achieving a TSR of about 15% is the necessary level to be

considered an attractive investment by investors. Achieving this means that the company's value will double in about

five years mathematically. However, when looking at the performance of the TSR over the past five years, while the

average of the Global Top exceeds the 15% TSR level, almost all Japanese listed pharmaceutical companies, except for

a very few high-performing companies, are falling below this level (Figure 3).

When evaluating the Price-to-Book Ratio (PBR) of the Japanese listed pharmaceutical companies, the proportion of

companies with a PBR of less than 1x (companies where the market capitalization is below the net asset value) was

10% in 2000, but has reached about 45% in 2023. In other words, nearly half of the Japanese listed pharmaceutical

companies are "destroying shareholder value, and it would be better to dissolve than continue operations, even in a state

of disqualification for listing." Low PBR is an issue seen across Japanese companies, and in late March 2023, the Tokyo

Stock Exchange issued improvement requests to low-PBR companies.

Source: FactSet

*1: weighted average

TSR 15%

TSR trend with 2018.01 as 100 (multiple, 2018.01-2022.12)

FIGURE 3: CHANGES IN STOCK PRICES OF LISTED JAPANESE PHARMACEUTICAL COMPANIES

AND GLOBAL TOP LEADERS

0

50

100

150

200

250

300

350

400

450

2022.12

2020.12

2018.12

2018.01 2019.12 2021.12

Weighted

average of

Global Top

Attractive

to invest

Not

attractive

to invest