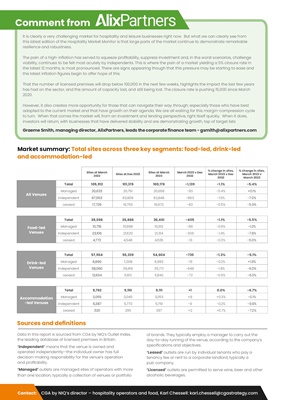

Sites at March

2022

Sites at Dec 2022

Sites at March

2023

March 2023 v Dec

2022

% change in sites,

March 2023 v Dec

2022

% change in sites,

March 2023 v

March 2022

All Venues

Total 105,912 101,315 100,176 -1,139 -1.1% -5.4%

Managed 20,633 20,751 20,658 -93 -0.4% +0.1%

Independent 67,553 63,809 62,846 -963 -1.5% -7.0%

Leased 17,726 16,755 16,672 -83 -0.5% -5.9%

Food-led

Venues

Total 38,596 36,866 36,461 -405 -1.1% -5.5%

Managed 10,718 10,698 10,612 -86 -0.8% -1.0%

Independent 23,106 21,620 21,314 -306 -1.4% -7.8%

Leased 4,772 4,548 4,535 -13 -0.3% -5.0%

Drink-led

Venues

Total 57,554 55,339 54,604 -735 -1.3% -5.1%

Managed 6,860 7,008 6,993 -15 -0.2% +1.9%

Independent 38,060 36,419 35,771 -648 -1.8% -6.0%

Leased 12,634 11,912 11,840 -72 -0.6% -6.3%

Accommodation

-led Venues

Total 9,762 9,110 9,111 +1 0.0% -6.7%

Managed 3,055 3,045 3,053 +8 +0.3% -0.1%

Independent 6,387 5,770 5,761 -9 -0.2% -9.8%

Leased 320 295 297 +2 +0.7% -7.2%

Sources and definitions

Data in this report is sourced from CGA by NIQ's Outlet Index,

the leading database of licensed premises in Britain.

'Independent' means that the venue is owned and

operated independently-the individual owner has full

decision-making responsibility for the venue's operation

and profitability.

'Managed' outlets are managed sites of operators with more

than one location, typically a collection of venues or portfolio

of brands. They typically employ a manager to carry out the

day-to-day running of the venue, according to the company's

specifications and objectives.

'Leased' outlets are run by individual tenants who pay a

tenancy fee or rent to a corporate landlord, typically a

pub company.

'Licensed' outlets are permitted to serve wine, beer and other

alcoholic beverages.

Market summary: Total sites across three key segments: food-led, drink-led

and accommodation-led

Comment from

It is clearly a very challenging market for hospitality and leisure businesses right now. But what we can clearly see from

this latest edition of the Hospitality Market Monitor is that large parts of the market continue to demonstrate remarkable

resilience and robustness.

The pain of a high-inflation has served to squeeze profitability, suppress investment and, in the worst scenarios, challenge

viability, continues to be felt most acutely by independents. This is where the pain of a market yielding a 5% closure rate in

the latest 12 months, is most pronounced. There are signs appearing though that this pressure may be starting to ease and

the latest inflation figures begin to offer hope of this.

That the number of licensed premises will drop below 100,000 in the next few weeks, highlights the impact the last few years

has had on the sector, and the amount of capacity lost, and still being lost. The closure rate is pushing 15,000 since March

2020.

However, it also creates more opportunity for those that can navigate their way through; especially those who have best

adapted to the current market and that have growth on their agenda. We are all waiting for this margin-compression cycle

to turn. When that comes the market will, from an investment and lending perspective, right itself quickly. When it does,

investors will return, with businesses that have delivered stability and are demonstrating growth, top of target lists

Graeme Smith, managing director, AlixPartners, leads the corporate finance team - gsmith@alixpartners.com

Contact: CGA by NIQ's director - hospitality operators and food, Karl Chessell: karl.chessell@cgastrategy.com