Hospitality loses one in 18 sites after rocky year

1. Market overview

Introduction by Karl Chessell, CGA by NIQ director - hospitality operators and food, EMEA

After a tough first half of 2023 for businesses and consumers alike,

our latest Hospitality Market Monitor sets out the mixed impacts

on Britain's licensed sector. It shows a 1.1% contraction in site

numbers over the last quarter to a little over 100,000 sites, and if

current trends continue the total will drop from six figures into five

for the first time since the Monitor began.

The 1,139 net closures and associated job losses between March

and June have been distressing for all those involved. Soaring

costs in energy, food, labour and more inputs have worn away

businesses' profit margins, and high inflation and interest rate

rises have weakened consumer confidence.

Despite this, some key indicators remain positive. The Coffer

CGA Business Tracker has recorded year-on-year growth in sales

at managed pubs, bars and restaurants in every month of 2023

so far, while the CGA and Fourth Business Confidence Survey

indicates leaders' optimism has increased since the start of the

This edition of the Hospitality Market Monitor shows Britain had

100,176 licensed premises at the end of June 2023. It represents

a net decline of 1,139 sites over the second quarter of 2023, and

of 5,736 sites over the last 12 months. Put another way, Britain has

lost around one in 18 of its licensed premises since June 2022.

This extends a long-term downward trend that was dramatically

accelerated by COVID-19. Since the pandemic hit in early 2020,

Britain has seen a net decline of 14,932 sites-13.0% of the

pre-COVID total. Smaller businesses have borne the brunt, and

76.5% of all these net closures have been in the independent

sector. By contrast, the managed segment has only 3.7%

fewer sites than it did pre-COVID.

However, it's not all doom and gloom. Total net closures in the

first half of 2023 (1,895) were less than half the number seen in

the second half of 2022 (3,841), and many units that have been

vacated recently have been swiftly reoccupied by other

operators-often emerging multi-site groups. Of course, it

remains to be seen whether this slowdown continues or whether

relentlessly high costs force more closures over the remainder

of 2023.

As this table shows, some segments have been more resilient

than others in the last 12 months. Casual dining (down 5.6%

since June 2022) has been hit harder than most, with several

major brands seeking to consolidate their estates. There have

also been steep drops in sports and social bars (down 6.5%) and

nightclubs (down 12.2%), though closures in the latter may be

bottoming out (see page 2).

Other channels including pubs have held up better. Food-led

pubs (down 2.9% since June 2022), high street pubs (down 3.1%)

and community pubs (down 4.1%) have all recorded notably

fewer closures than the sector as a whole-a welcome sign that

consumers are still eager to drink out.

year. We have also seen the tide starting to turn on inflation in the

UK with the latest figures showing the rate of inflation slowing. As

we see on page 2, market segments including city centres and

bars remain robust. More venue closures are likely while costs

remain so high, but the outlook for well-resourced, distinctive

and customer-focused groups remains good.

HospitalityMarketMonitor

JULY 2023

Issue 39

Review of GB pub, bar and restaurant supply

77YEARS

B R I N G I N G Y O U D A T A A N A L Y S I S

Sites at

June 2022

Sites at

March 2023

Sites at

June 2023

% change in sites,

June 2023 v March 2023

% change in sites,

June 2023 v June 2022

% change in sites,

June 2023 v March 2020

Bar 4,544 4,457 4,413 -1.0% -2.9% -3.1%

Bar restaurant 3,380 3,242 3,206 -1.1% -5.1% -13.0%

Casual dining restaurant 5,381 5,160 5,082 -1.5% -5.6% -23.3%

Community pub 18,948 18,254 18,172 -0.4% -4.1% -11.1%

Food pub 12,055 11,754 11,702 -0.4% -2.9% -7.1%

High street pub 6,232 6,040 6,040 0.0% -3.1% -9.3%

Hotel 7,464 7,264 7,269 +0.1% -2.6% -6.5%

Large venue 4,550 4,519 4,263 -5.7% -6.3% -7.8%

Nightclub 994 865 873 +0.9% -12.2% -30.0%

Restaurant 16,372 15,350 15,192 -1.0% -7.2% -19.1%

Sports / social club 21,364 20,317 19,974 -1.7% -6.5% -12.3%

Total 105,912 101,315 100,176 -1.1% -5.4% -13.0%

Outlets by segment, June 2023 v March 2023 and June 2022

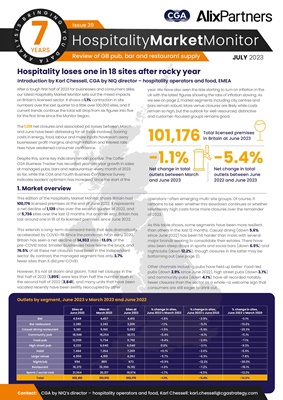

101,176

-1.1% -5.4%

Total licensed premises

in Britain at June 2023

Net change in total

outlets between March

and June 2023

Net change in total

outlets between June

2022 and June 2023

Contact: CGA by NIQ's director - hospitality operators and food, Karl Chessell: karl.chessell@cgastrategy.com