City centres

The late-night market

After months of lockdowns and restrictions, city centres have

steadily welcomed back office workers and visitors in the last

12 months, with positive results for hospitality.

Data for this edition of the Hospitality Market Monitor shows a

4.2% net fall in licensed premises in Britain's city centres in the

12 months to June 2023. This is a better figure than the drops

of 5.9% and 5.4% in large and small towns respectively over

the same period.

Cities are increasingly drawing in people from the suburbs

and 'satellite' towns-not just to workplaces after an extended

period of working from home, but for leisure too. They have also

benefited from a growth in city centre residents. A wave of

residential developments in cities like Manchester, Liverpool

and Leeds over the last few years has increased the target

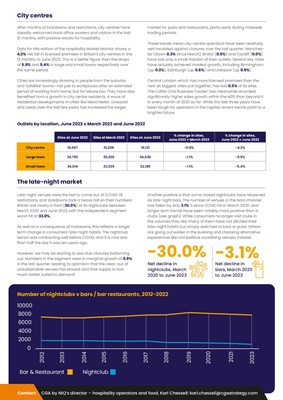

Late-night venues were the last to come out of COVID-19

restrictions, and lockdowns took a heavy toll on their numbers.

Britain lost nearly a third (30.0%) of its nightclubs between

March 2020 and June 2023, with the independent segment

worst hit at 33.0%.

As well as a consequence of lockdowns, this reflects a longer

term change in consumers' late-night habits. The nightclub

sector was contracting well before COVID, and it is now less

than half the size it was ten years ago.

However, we may be starting to see club closures bottoming

out. Numbers in the segment were in marginal growth of 0.9%

in the last quarter, leading to optimism that the clear-out of

unsustainable venues has slowed, and that supply is now

much better suited to demand.

market for pubs and restaurants, particularly during midweek

trading periods.

These trends mean city-centre operators have been relatively

well insulated against closures over the last quarter. Manchester (down 0.3%

since March), Bristol (0.5%) and Cardiff (0.0%)

have lost only a small fraction of their outlets. Several key cities

have actually achieved modest growth, including Birmingham

(up 0.3%), Edinburgh (up 0.6%) and Liverpool (up 0.9%).

Central London, which has more licensed premises than the

next six biggest cities put together, has lost 0.5% of its sites.

The Coffer CGA Business Tracker has meanwhile recorded

significantly higher sales growth within the M25 than beyond it

in every month of 2023 so far. While the last three years have

been tough for operators in the capital, recent trends point to a

brighter future.

Another positive is that some closed nightclubs have reopened

as late-night bars. The number of venues in the bars channel

has fallen by only 3.1% % since COVID hit in March 2020, and

longer term trends have been notably more positive than in

clubs (see graph). While consumers no longer visit clubs in

the volumes they did, many of them have not ditched their

late-night habits but simply switched to bars or pubs. Others

are going out earlier in the evening and choosing alternative

experiences like competitive socialising venues, instead.

Number of nightclubs v bars / bar restaurants, 2012-2022

10000

Sites at June 2022 Sites at March 2023 Sites at June 2023

% change in sites,

June 2023 v March 2023

% change in sites,

June 2023 v June 2022

City centre 10,567 10,206 10,121 -0.8% -4.2%

Large town 36,792 35,026 34,638 -1.1% -5.9%

Small town 34,014 32,535 32,189 -1.1% -5.4%

Outlets by location, June 2023 v March 2023 and June 2022 -30.0% -3.1%

Net decline in

nightclubs, March

2020 to June 2023

Net decline in

bars, March 2020

to June 2023

8000

6000

4000

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2023

2000

Bar & Restaurant Nightclub

0

Contact: CGA by NIQ's director - hospitality operators and food, Karl Chessell: karl.chessell@cgastrategy.com